Updated May 2026

What Is Full Coverage Insurance?

Full coverage combines three separate insurance types: liability (pays for damage you cause to others), collision (pays for your vehicle damage in crashes), and comprehensive (pays for theft, weather, vandalism, and animal strikes). You cannot buy 'full coverage' as a single product — it is the result of purchasing all three types together on one policy. Most lenders require it on financed vehicles, and many drivers keep it long after the loan is paid to protect the asset value.

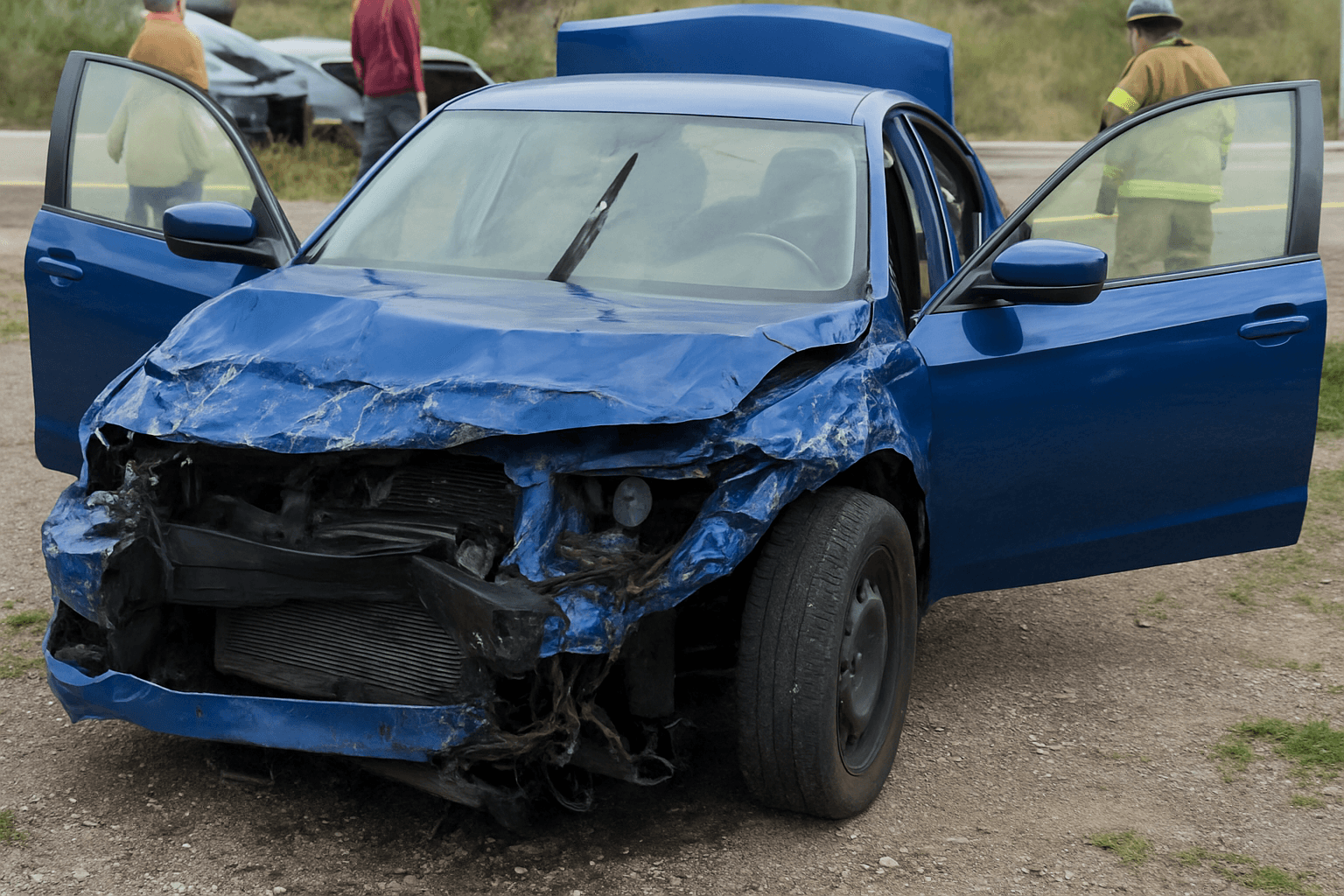

- The other driver has $9,000 in medical bills and $6,500 in vehicle repair costs. Your car sustains $4,200 in front-end damage. Liability coverage pays the $15,500 you owe to the other driver. Collision coverage pays the $4,200 for your vehicle, minus your deductible. Without collision, you pay the $4,200 out of pocket.

- A severe storm causes $5,800 in dent and glass damage to your vehicle. Comprehensive coverage pays the repair cost minus your deductible — typically $500 or $1,000. This type of damage is not covered by collision or liability. If you carry only liability insurance, you pay the full $5,800 yourself or drive the vehicle damaged.

- The at-fault driver has only the state minimum liability limit of $25,000, but your vehicle is worth $32,000. Their insurance pays $25,000. Your collision coverage pays the remaining $7,000 minus your deductible, then your insurer pursues the at-fault driver for reimbursement. Without collision, you absorb the $7,000 shortfall and must negotiate directly with the other driver.

How Much Does Full Coverage Insurance Cost?

Full coverage typically adds $80 to $180 per month compared to liability-only for drivers 75 and older, depending on vehicle value, deductible, and claims history. Annual cost ranges from $960 to $2,160 above the liability-only base premium.

- Vehicle replacement value — higher-value vehicles cost significantly more to insure for collision and comprehensive because the insurer's payout risk increases with asset value.

- Deductible selection — choosing a $1,000 deductible instead of $500 reduces monthly premiums by $15 to $30, but increases out-of-pocket cost at claim time.

- Garaging zip code — urban areas with higher theft and vandalism rates increase comprehensive premiums, while rural areas with more animal strikes show different risk profiles.

- Claims history in the past 3 to 5 years — any at-fault collision or comprehensive claim raises rates significantly, and multiple claims can trigger non-renewal at age 75-plus.

- Credit-based insurance score — in states where it is permitted, a lower score increases premiums for collision and comprehensive more than for liability alone.

- Annual mileage — drivers reporting under 5,000 miles per year may qualify for low-mileage discounts that offset a portion of the collision premium increase.

See How Much You Could Save

Get personalized full coverage insurance quotes in minutes.

Who Needs Full Coverage Insurance?

Drivers 75 and older should keep full coverage if their vehicle is worth more than $8,000 and they cannot afford to replace it out of pocket after a total loss. It is also essential if you still owe money on the vehicle — lenders require it until the loan is paid. Maintaining full coverage continuously matters because dropping to liability-only and later adding collision back often triggers higher rates or underwriting scrutiny, and some carriers limit reinstatement options for drivers over 80.

Calculate your vehicle's current market value using resources like Kelley Blue Book or NADA Guides. Compare that to your annual collision and comprehensive premium plus your deductible. If the coverage costs more than 20 percent of the vehicle's value per year, and you have enough savings to replace the car, dropping to liability-only makes financial sense. If you cannot replace the vehicle without financing — and requalifying for a loan at 75-plus is difficult — keep full coverage.